Retirement Plan Required Minimum Distributions

by Steve Goodman

CPA, MBA – President & Chief Executive Officer

Contact Steve today for more info.

The US Government has established multiple retirement plans allowing one to save money on a pre-tax basis. Consider a person in the 40% marginal tax bracket (federal and state combined). If someone can move $10,000 from salary to a qualified pre-tax money savings program, this person can save $4,000 in immediate taxes. The money can grow tax-deferred for many years. When the account owner retires intending to live off these savings, their marginal tax rate may have declined. Even if the new marginal tax rate is 30%, the account owner has saved $1,000 while enjoying tax deferred growth for many years.

When one reaches retirement, Uncle Sam requires that you start paying taxes on the tax-deferred retirement accounts. The collection mechanism is a forced withdrawal from these accounts that becomes a taxable event. These withdrawals are known as Required Minimum Distributions or RMD’s.

The Basics

When discussing RMD’s, we separate the universe of common retirement plans into three categories:

- IRA’s, SIMPLE IRA’s, and Sep-IRA’s

- 401(k) plans and their non-profit equivalents

- Roth IRA’s

Defined benefit programs are the fourth category of retirement plans. Please see the article ‘Defined Benefit Plans for Small Businesses and the Self Employed’ by S. Goodman and other defined benefit articles.

The following rules apply to all pre-tax IRA’s, and most company IRA plans for the original owner of these plans.

When you must start RMD’s – You may begin withdrawing money from these accounts without incurring a tax penalty in the year you turn 59½. You must begin to withdraw money from these accounts by April 1 of the calendar year following the year in which the account owner turned 70½.By example: An account owner’s 70th birthday is on September 15, 2018. The account owner’s 70½ birthday is six months later or March 15, 2019 (using a 30 day month, 360-day year calculation). The 1st RMD must be made by April 1, 2020.

What if the account holder is still working? – For IRA’s, the rule stands. You must start taking withdrawals.

Once one starts taking distributions, must they continue? – Yes, until they die or deplete the accounts. Annual RMD’s are required by December 31 following the year the account holder turned 70½. If someone defers taking the RMD until late March the following year he/she turns 70½, a second distribution will be required for the next birthday in the same calendar year. Two distributions in the same calendar year could result in paying a higher tax rate on the second distribution.

There is a rule change in the case of 401(k)’s and some non-profit equivalents for the original owner of these plans.

What if the account holder is still working? –For 401(k)’s and some company plans with IRS approved conditions, you may be able to defer taking distributions.

In the case of Roth IRA’s, there is no RMD for the original owner of these plans. All Roth IRA distributions, assuming the account is at least five years old, are tax-free.

Calculating RMDs

How does one figure the amount of RMD? – The easy answer is a three-step process. Of course, there are exceptions.

- Identify every retirement account – determine which ones are subject to an RMD based on the type of account, your age, work status, and account specific terms and conditions.

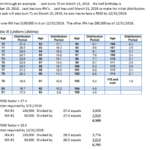

- Identify the market value of each account as of the prior’s year December 31. In most cases, this is simply a matter of looking at the annual statement. If you have a retirement account invested in non-marketable securities, you may need an expert’s assessment.

- Look up the distribution factor in the IRS tables (“Uniform Lifetime Table”) and multiply the December 31 account balances by the factor. This is your RMD by account.

Exceptions to the rules

- If the company sponsored retirement savings program contains IRS approved wording that extends the RMD date until retirement, the plan terms and conditions take precedence provided the account holder is working beyond 70½.

- If a person is a 5% or more owner of the company sponsoring a retirement plan with the extension wording, then the wording does not apply for this individual.He/she must abide by the 70½ regulation.

- If the account holder dies, see ‘What if the account holder dies?’section in this paper.

An example of the RMD computation is as follows.

Does it matter how or where one takes the RMD’s? – When taking RMD’s from accounts, one must categorize all your retirement accounts into one of four buckets:

- Your IRA’s and other defined contribution accounts

- Your 401(k)’s

- Spouse’s IRA’s and other defined contribution accounts

- Spouse’s 401(k)’s

Within the two IRA buckets, you can mix and match within buckets. Assume you have combined IRA RMD of $4,000 and your spouse has a combined IRA RMD of $3,000. You can take your $4,000 from any combination of IRA’s in your bucket. And your spouse can do the same in your spouse’s bucket. For IRA RMD purposes, all that matters are whose name is on the account and that the distributions meet or exceed the RMD’s every year in total within the buckets.

401(k)’s and 457(b)’s are treated differently. If you have multiple 401(k)’s or 457(b) plans, you must take at least the RMD from each account.

403(b) plans can be aggregated among themselves as if they were a separate bucket. If someone has multiple 403(b) plans, the RMD can be taken from any or all of the 403(b) plans.

Can I take an RMD in something other than cash? – Yes, you can take a withdrawal ‘in kind’. If you have invested your account in a venture or fund that permits asset distribution, the government has no problem with you receiving land, stock, or some other asset as a distribution. On the positive side, an asset distribution avoids the necessity to sell the asset. On the negative side, asset transfers are much more complex than cutting a check. You must be prepared to justify the value of the asset to the IRS if called upon to do so. You also must either have the cash to pay the taxes due or incur sales costs to convert some or all the in-kind asset into cash to pay the taxes due.

Special rules for Roth IRA’s – Roth IRA’s are after-tax money. Assuming the account holder has held the account for at least 5 years and is at least 59½ years old, the account holder can take any distribution or no distribution at any time. There is no RMD on a Roth IRA for the original owner of the account. A spouse who inherits a Roth IRA also has no requirement to take a distribution. A non-spousal beneficiary, including a child, must take distributions based on their life expectancy, though all distributions are not taxable providing the Roth IRA is at least five years old.

What if the account owner dies? – There are different rules for how an IRA or 401(k) is treated depending upon who the beneficiary is and how old the account owner was at death. In the year of the account owner’s death, the RMD is based on the now deceased owner’s age in the year of his/her death. Going forward, the following rules are taken from the IRS.

From the IRS Retirement Topic series.

https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmds

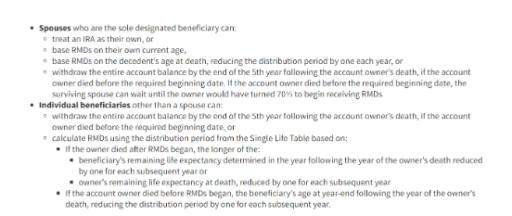

The spouse has several options. We consider an example Let’s consider a husband who passes away at 78, having not taken a distribution. The wife is 73 at the time of her husband’s death. She has the following options:

- She can treat the IRA as if it was hers all along. She would use her age to compute the coming year’s RMD. If she was only 67 years old, she would not have to take an RMD until she turned 70½ years old. In our example, this would work in her favor as the RMD at 78 is higher than the RMD at 73 allowing her to take a smaller RMD if she chooses.

- She can calculate her RMD based on her husband’s age assuming he was still alive. In our example, this is the opposite of the point above. This option raises her RMD which is not beneficial.

- If her husband died before the required distribution date, she can withdraw all the funds over the 5 calendar years from the date of his death. She can take these withdrawals as taxable distributions or roll them over into an IRA in her name. In our example, her husband died after his required distribution date, so this option does not apply.

A non-spouse beneficiary has a few fewer options. Let’s assume a 45-year-old daughter of the deceased is the beneficiary of the retirement plan.

- If the account owner died before the required distribution date (which is not the case in our example), the daughter has 5 years to withdraw the entire amount. This is the 5 Year Rule of inherited plans. Alternatively, she may roll the account balance into an IRA in her name. She must then follow the IRS guidelines for RMD’s.

- Since our account owner died at 78, 7+ years after his required distribution date, the daughter must make RMD’s based on the length of two alternatives:

- The daughter’s life expectancy as based on the IRS Single Life Expectancy Table reduced by one each subsequent year or

- The owner’s remaining life expectancy at the age of his death reduced by one each subsequent year.

Since the daughter is only 45 compared to the owner’s age of 78 at the time of death, her life expectancy is the longer of the two. She must roll the inherited IRA into a special class of IRA called an Inherited IRA in her name. This alerts the IRS as to the status of the account.

For non-spouse beneficiaries eligible for the 5 Year Rule, inherited accounts are not subject to a 10% early withdrawal penalty. The beneficiary may contribute to the inherited IRA but must empty the account by the end of Year 5. Rollovers from the inherited IRA to a new IRA in the beneficiary’s name are permitted.

If the inherited IRA is a Roth IRA, the rules are a bit different. Roth IRA’s have a mandatory 5-year holding period to withdraw gains tax-free. These accounts are also subject to the 5 Year RMD Rule. If the inherited account was only 3 years old when the account holder died, the beneficiary needs another two years to withdraw gains tax-free. Yet the beneficiary must make RMD’s to drain the account over the first 5 years following the inheritance. In this circumstance, the assistance of a tax professional is recommended.

Failure to take RMDs – If one does not take an RMD, the IRS can penalize the account holder up to 50% of the RMD. So, if an account holder has a $5,000 annual RMD, but failed to take the distribution, the IRS can impose a $2,500 penalty. The IRS has an appeals process just for this penalty.

Roll-over of excess distribution – In year X, an individual had an RMD of $10,000.He/she took $14,000 that year. Can he/she apply the excess $4,000 to another year’s RMD? No. Each year is calculated separately solely based on account valuations on December 31 and the appropriate IRS tables based on life expectancy.

CPA, MBA – President & Chief Executive Officer

About Steve Goodman

For more than 30 years, Steven has provided insightful solutions to the challenges of business succession, wealth preservation and charitable planning, focusing on the needs of owners of closely held businesses and high net worth individuals.

He's been featured in the New York Times and is an accomplished speaker and has presented over the years to many organizations and professional groups on efficient business succession, estate planning issues and tax strategies. Steven is a CPA who was vice president of the Trust and Investment Division of JP Morgan Chase and a supervisor for KPMG Peat Marwick, and holds an MBA from Fordham University.