Role of Annuities in Retirement Planning

by Steve Goodman

CPA, MBA – President & Chief Executive Officer

Contact Steve today for more info.

History

The recession of 2000 – 2001 convinced many corporations to eliminate their defined benefit programs for their employees. Declining stock prices, compounded by ERISA requirements that companies catch up with unfunded plan liabilities, devastated company earnings, and valuations. The shift from defined benefit programs to defined contribution shifted the risks of retirement income, longevity, and planning from employer to employee.

The result of the shift has been to create the first generation of retirees in many decades with a critical need to plan their own retirements. Experts in the field of retirement planning recognize that far too many people are approaching retirement age with drastically underfunded retirement savings.

Retirement Planning Tools

There are two primary retirement planning options. The first is a retirement calculator. The internet offers dozens of calculators with complexity levels ranging from simple to Monte Carlo simulations. Many are inexpensive or free. All suffer from the same concern – the output is largely a function of the assumptions employed in the computation. Most self-directed users employ assumptions reflecting current conditions. Models that use historical data may offer more detailed results including probabilities that retirement income will be insufficient.

Recognizing that past performance is not a guarantee of future performance, many calculators look at averages without accounting for risk.

The alternative is to engage a financial planner who specializes in retirement planning. A planner’s job is one of risk management. While identifying how much cash a person or family requires during their retirement, the planner needs to account for the following risks.

- How much risk is appropriate to obtain the required capital for a comfortable retirement?

- What if the retiree lives to a very old age?

- What if inflation increases significantly?

Planners employ a strategy of subdividing the planning horizon into manageable sections. Two examples are provided. Example 1 divides the financial requirement by type of capital: required, contingency, and desired. The second example looks at the same financial requirement in terms of time. Both deal with the same risks and many of the same products, though the weightings on each may be different.

Example 1 – The three-sector approach

The three-sector approach divides the retiree’s needs in minimum guaranteed income, conservative yet flexible income, and desired additional income.

Minimum Guaranteed Income – This category accounts for a base level of income. It needs to provide sufficient income to cover basic living expenses. Income in this category should meet two requirements; inflation protected and guaranteed for life. Taken together, income in this category provides protection from inflation, rising interest rates, and longevity. Income sources for this category include Social Security and any defined benefit pensions available to the retiree. Pensions are not inflation protected. When computing their value, their payouts will decline in real dollars over time.

Retirees needing additional income in this category are candidates for an annuity. The annuity should come from a highly rated company even if it means the sacrifice of a few dollars each month. This category seeks guaranteed income with minimal risk. The annuitant’s primary concern should be the guaranteed payout. Annuitants will want to compare the payout options available. For a couple, the choices begin with a single life annuity or a joint survivorship option that pays until the passing of both people. After selecting a survivorship alternative, the annuitant needs to consider options concerning period certain and return of principal payouts. The annuitant must determine his/her ability to sacrifice some payout while the annuitant(s) live versus benefits for heirs when they pass on.

Conservative yet Flexible Income – Capital in this category is a step above required. These are funds invested in liquid investments for unexpected large expenses such as medical expenses. Liquidity allows for access as needed. Investments in dividend-paying equities and bonds, especially Treasury Inflation-Protected Securities (TIPS) provide for some pass through to heirs after death.

Longevity annuities play a role in this category. The retiree can use these specialized annuities to provide additional leeway in securing income in the Minimum Guaranteed Income category. Longevity annuities magnify a retiree’s investment by using the pooling of assets from other retires. As others in the cohort pass away, part of their principal and accumulated gains remains in the pool to enhance returns for those that remain.

Longevity annuities typically offer fewer payout options than other annuity types. Annuitants have the following payout decisions to make; how many lives will be covered (annuitant only or annuitant and spouse), will heirs receive any payments if the annuitant(s) dies soon after payouts commence, and whether or not to purchase a cost of living rider. As an example, an annuitant may select a return of principal guarantee for a husband and wife. As long as either the husband or wife is alive, they will receive payments. If upon both their passing, the couple did not receive at least the value of their original investment, then their

heirs will receive payments until the original principal is paid out. Annuitants need to recognize that each benefit has a cost in reduced payouts.

Desired Additional Income – This category provides for life’s extras. Many people also have a Defined Contribution plan. Coupled with personal assets such as a home and non-retirement savings, these assets can be invested in higher risk investments. These riskier investments can provide incremental benefit to improve the retiree’s lifestyle. Failure of these assets to achieve significant gains will not jeopardize the retiree’s ability to meet routine and some level of unplanned expenses.

Example 2 – the two sector time approach.

This methodology looks at the retirement challenge as having two-time components – a near term of retirement to 85, and then a longevity segment from 85 until expiration.

Retirement to 85 – Planning for this typically 20±5 year time frame is simplified by multiple factors. Longevity planning is deferred to the 85+ time period. Inflation may be a problem towards the end of the period. For the first few years, inflation is unlikely to change substantially from current levels. While inflation remains a planning concern, it is not an open-ended problem due to the limited duration of this planning period.

The retiree likely has some recurring income expected during the retirement to the 85-time frame. If those sources do not provide sufficient income, the finite nature of this period allows the planner to ladder bonds into the time frame. If the planning period consists of 20 years, the planner can select bonds redeemable in 20, 19, 18 and so on years down the road. Assuming a normal yield curve, the longer the bond has to redemption, the higher the effective interest rate.As the bonds come due, they provide a stream of capital for the coming year.

The same finite period does not provide a sufficiently long enough period for risk assets to work through any sequence of return problems. Therefore, equities are not a suitable candidate for investments in this time frame.

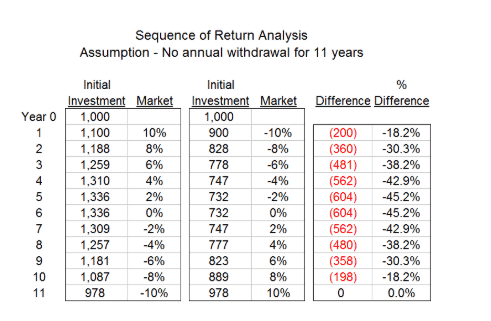

Consider the following charts. Each depicts an equity portfolio with annual investment returns ranging from +10% to -10%. The first chart assumes there is no annual cash withdrawal from the portfolio.

Regardless of how the returns are sequenced, lowest to highest or highest to lowest, the net result after 11 years is the same number.If one were looking at the portfolio value during the 11 year period, one might observe a nearly 30% drawdown of principal in the second case. Sequenced lowest to highest, the portfolio that began at $1,000 approaches $730 after five years of negative returns. While five negative years is unusual in market history, a 30% drawdown is not as unusual.

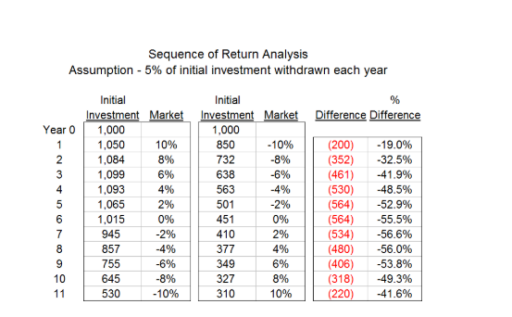

If one withdraws a portion of the portfolio each year, the outcomes change considerably. Now the sequence of returns matters greatly. It also a matter of concern if the annuitant is making a series of payments over time. The difference in portfolios over just 11 years is 530 vs 310, a 41% reduction in residual value. One cannot comfortably employ an equity portfolio to fund a ~20 year time period. The sequence of returns could play a critical role in determining the cash available to pay fixed and contingency expenses towards the end of the period.

85 to Expiration – Planning for this time period is complicated by unknown longevity. Were the period finite, the planner’s job would be much easier. There are two strategies available to the planner. The first is the purchase of a longevity annuity at the time of retirement. The approximately 20 year accumulation period allows the retiree to limit his/her financial commitment to the longevity annuity.

The longevity annuities primary job is to provide income while the annuitant and spouse are alive. By eliminating payments to heirs and all riders, with the exception of a cost of living rider, the retiree will receive the maximum monthly payment per $1,000 invested. Many people are unable to accept the draconian use-it-or-lose-it conditions upon which the longevity annuity was developed. For these people, they will want to evaluate some period certain options. Given the extended time from principal payment to the final payout, one cannot assume that inflation will remain under control. An annuitant should consider transferring this risk to the insurer via a cost of living rider.

The alternative solution is to invest the capital needed for this time period in equities. The same extended horizon that justifies purchasing a cost of living rider on an annuity works in the retiree’s favor in an equity portfolio. For the first ~20 years, the retiree has no need to withdraw cash from this portfolio. His/her needs for the first 20 years were addressed in the Retirement to 85 periods. This provides the time for the sequence of return risk to largely dissipate.

Studies have shown that over almost every 20 year period, but certainly every 35 year period in the last 150 years, equities have outperformed the effective interest currently offered by longevity annuities. Past performance is not a guarantee of future results. If this were to hold true going forward, then the equity portfolio would be the preferred investment vehicle for multiple reasons:

- Capital gains versus ordinary income taxes. Some dividends and all capital gains receive preferential tax treatment.

- Capital to leave to heirs. If one can avoid selling the entire portfolio to meet longevity needs, the remaining portion is available for the annuitant’s heirs. The heirs will enjoy an untaxed step up in basis when they receive these securities.

- Flexibility and access during the accumulation period. Equities are easily, quickly, and cheaply converted to cash, if necessary.

Use of a longevity annuity in retirement planning provides the flexibility to invest other funds in higher risk, higher return alternatives, such as equities. The longer the accumulation period, the less one must allocate to the elimination of outliving one’s capital.

Annuities may not be an optimal solution for every retiree, but for many, they are part of the discussion. Annuities offer tax deferral, guaranteed longevity, cost of living riders, and, in the case of fixed and index annuities, simplicity. Longevity annuities use pooling to offer yields unavailable from other minimal-risk investments. They have a role to play in retirement planning.

CPA, MBA – President & Chief Executive Officer

About Steve Goodman

For more than 30 years, Steven has provided insightful solutions to the challenges of business succession, wealth preservation and charitable planning, focusing on the needs of owners of closely held businesses and high net worth individuals.

He's been featured in the New York Times and is an accomplished speaker and has presented over the years to many organizations and professional groups on efficient business succession, estate planning issues and tax strategies. Steven is a CPA who was vice president of the Trust and Investment Division of JP Morgan Chase and a supervisor for KPMG Peat Marwick, and holds an MBA from Fordham University.